Zoning Laws: A Practical Guide

Why does zoning matter? Zoning regulations dictate the types of buildings that can be constructed, whether existing properties can be used for different purposes, and if current structures can be replaced with new ones.

read more

Five Key Factors to consider when buying your next Residential Investment Property

Real estate books and social media experts are always telling everyday investors that...

read moreUnlocking Exclusive Property Deals: REI Magazine

View the online article published in Real Estate Investor Magazine - June 2024

read moreIs property investing only for the wealthy?

Property ownership has always been associated with wealth. Property is a tangible asset that can be seen, providing a sense...

read more5 Rules for Property Flipping

Property flipping is big business in the USA, and the bug has bitten in South Africa. There are no barriers to entry; anyone can jump in and do a flip. Here are my five top rules for a successful property flip...

read moreLandlord insurance – is it worthwhile?

Tenant defaults are a landlord’s nightmare. It impacts your cash flow, and if the situation drags on, evictions can be very costly...

read moreSelecting the type of property investment that’s right for you

When it comes to property investing, we’re spoilt for choice. So before you start physically looking at properties, narrow down the options by considering what type of investment will best suit you.

read moreThe upside of a high interest rate environment

Interest rates have risen sharply over the past few months and this may instinctively feel negative as the cost of borrowing money increases....

read moreStaging sells

When selling a property, first impressions count. According to the National Association of Realtors in the USA, around 50% of agents say that staged homes sell faster and....

read moreBest property for investment?

There’s an old saying that when buying property the three most important factors to consider are location, location and location. However ...

read moreDrab to fab – Three ways to improve your property value.

The trick to achieving a great selling price is to create a home that someone will fall in love with and want to buy. But you don’t always have to spend a small fortune to make a big impact. Start by seeing what you can...

read moreNet Present Value (NPV): What You Should Know

What Is Net Present Value (NPV)? Net Present Value (NPV) is an investment performance measure widely used in finance and commercial real estate. NPV is the difference between the present value of all cash inflows and the present value of all cash outflows. NPV tells an investor whether the investment is achieving...

read moreIs AirBnB a good investment?

According to a survey by Airbnb in 2022, South African hosts earned just over R26,000 over a six month period, equivalent to around one month’s pay.

read more

Loan to Value Ratio (LTV): A Calculation Guide

Loan to Value Ratio (LTV): A Calculation Guide, by Robert Schmidt (PropertyMetrics).

read more

2023 Property Calendar (Download)

See the list of property related events for this year, with our Property Events Calendar 2023.

read more

-

Jason in Real Estate Investor

Born and raised in Cape Town, Jason Lee was educated at Wynberg Boys High. Today he is the head of Rawson Commercial...

read more -

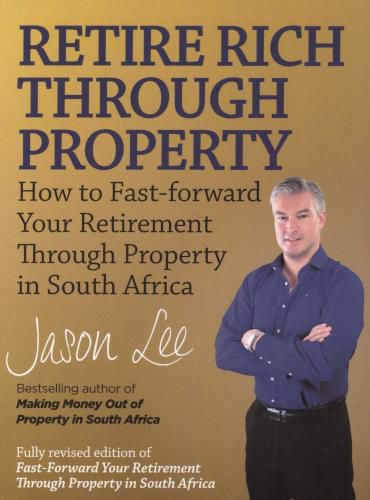

Book Review by Ian Mann

"Fast-Forward Your Retirement Through Property"

read more

...reviewed by Ian Mann